| BETTERMENT SPOTLIGHT | |

InvestorMint Rating 5 out of 5 stars |

via Betterment secure site

|

In this Betterment review, you will see how the platform has matured into one of the most capable robo-advisors available in 2026 — and whether its fees and features still hold up against a crowded field of competitors.

Betterment combines automated portfolio management with optional access to certified financial planners (CFPs), making it a practical fit for hands-off beginners and higher-balance investors who want occasional human guidance alike.

As of early 2026, Betterment manages more than $65 billion in assets for over 1 million customers — a dramatic increase from the $22 billion reported in earlier reviews — with client feedback remaining broadly positive across major review platforms.

From daily tax-loss harvesting and goal-based retirement planning to a no-fee high-yield cash account, Betterment remains one of the most complete robo-advisor platforms on the market and is still difficult to beat on price at the Digital tier.

Betterment Review 2026

Founded in 2008, Betterment now serves more than 1 million customers and manages over $65 billion in assets — numbers that reflect its standing as one of the most established robo-advisors in the U.S.

The platform goes well beyond basic automated investing. Core features include tax-loss harvesting, socially responsible investing (SRI), goal-based portfolio management, and access to certified financial planners (CFPs) on the Premium tier.

Pricing is straightforward. The Digital plan costs $5 per month or 0.25% annually — the flat fee applies to smaller accounts, while the percentage kicks in for balances above $24,000 or with $250+ in recurring monthly deposits. The Premium plan runs 0.65% annually and requires a $100,000 minimum, adding unlimited CFP access. Underlying ETF expense ratios range from 0.03% to 0.30%, charged by fund providers, not Betterment.

For hands-off investors who want professional-grade automation without paying traditional advisor rates, Betterment remains a compelling starting point.

Betterment Features at a Glance (2026)

Betterment now manages more than $65 billion for over 1 million customers. The table below summarizes current fees and core features across both the Digital and Premium tiers.

| Fees | Digital: 0.25%/yr or $5/mo; Premium: 0.65%/yr |

|---|---|

| Minimum Investment | $0 to open; $10 to begin investing |

| Tax-Loss Harvesting | Yes — all taxable accounts, monitored daily |

| Socially Responsible Investing | Yes |

| Live Advisors (CFPs) | Premium plan only ($100,000 minimum balance) |

| Portfolio Rebalancing | Yes — automatic |

| 401(k) Advice | Yes |

| Device Compatibility | Web, iOS, Android |

| Customer Support | Phone, Live Chat, Email |

| Promo | Earn up to $1,500 cash bonus on new investing accounts |

Fee fine print: The Digital plan’s $5/month flat fee applies when your balance is below $24,000 and you have no recurring monthly deposits of $250 or more; otherwise, the 0.25% annual rate kicks in. Balances above $1 million qualify for progressive discounts, dropping to 0.15% on the $1M–$2M portion and 0.10% above $2M. Betterment also charges a flat $75 outbound transfer fee per investing account.

Betterment Current Offer & Fee Snapshot

As of early 2026, Betterment is offering new customers a cash reward of up to $1,500 when you open an individual investing account and make a qualifying deposit. The older free-management deposit tiers have been replaced by this reward structure. Always confirm current terms on Betterment’s promotions page, as offers change periodically.

| Plan | Annual Fee | Minimum Balance |

| Betterment Digital | 0.25% (or $5/month if under threshold) | $0 ($10 to begin investing) |

| Betterment Premium | 0.65% | $100,000 |

The $5/month flat fee applies if your balance stays below $24,000 and you have less than $250 in recurring monthly deposits. Clear either threshold and the standard 0.25% annual rate kicks in automatically.

High-balance investors benefit from progressive fee discounts:

- $1M–$2M: Rate drops to 0.15% on that portion

- Above $2M: Rate drops to 0.10% on that portion

Underlying ETF expense ratios (0.03%–0.30%) and a $75 outbound transfer fee are separate charges to factor into your total cost.

➤ Free Guide: 5 Ways To Automate Your Retirement

Is Betterment Right For You?

Fee-conscious, hands-off investors focused on the long term will find Betterment a strong fit. Now managing over $65 billion for more than 1 million customers as of early 2026, it remains the benchmark other robo-advisors are measured against.

Betterment Digital charges $5/month for accounts below the threshold, or 0.25% annually once your balance exceeds $24,000 or you establish $250 or more in recurring monthly deposits — well below the 1%+ most traditional advisors charge. Investors with balances over $1 million receive progressive fee discounts, dropping to 0.15% on the $1M–$2M tier and 0.10% above $2M.

Investors who want human support can upgrade to Betterment Premium (0.65% annually, $100,000 minimum), which adds unlimited access to certified financial planners (CFPs) for comprehensive guidance on retirement, tax strategy, and assets held outside Betterment.

Betterment is best suited for:

- Beginners and hands-off investors

- Long-term and retirement-focused investors

- Cost-conscious investors leaving high-fee advisors

- Savers who want goal-based planning tools

RETIREMENT INVESTORS

Betterment lets retirement savers open dedicated IRA goals with allocations that automatically de-risk as the target date approaches. Bond-heavy income portfolios remain available for investors in or near retirement, and Betterment’s 2026 portfolio updates expand access to actively managed bond funds for broader fixed-income exposure — a meaningful improvement for income-focused accounts.

Betterment Fees

Betterment fees are tiered based on the plan selected. Here is what to expect in 2026:

- Betterment Digital – 0.25% annually (or $5/month for balances under $24,000 without a qualifying $250+ monthly recurring deposit). Covers automated portfolio management, rebalancing, tax-loss harvesting, and goal-based planning tools.

- Betterment Premium – 0.65% annually ($100,000 minimum balance). Adds unlimited access to certified financial planners (CFPs) for comprehensive advice, including retirement planning, backdoor Roth conversions, and tax-efficient asset transfers.

- Progressive fee discounts apply on both plans for high-balance investors: balances between $1M–$2M are charged just 0.15%, and balances above $2M drop to 0.10%.

Underlying ETFs carry their own expense ratios of roughly 0.03%–0.30%, charged by fund providers and not collected by Betterment. A flat $75 fee applies to outbound account transfers. Crypto portfolios carry a separate 1% annual management fee on top of embedded trading costs.

Betterment Investment Method: How Portfolios Are Built

Betterment’s Core portfolio has delivered over 9% composite annual time-weighted returns after fees since launch, according to the company.

Betterment Investing Review: The platform’s investment philosophy draws on the work of Nobel laureates Robert Shiller and Eugene Fama, grounding its approach in modern portfolio theory and broad diversification.

Betterment builds portfolios from low-cost ETFs spanning approximately 12 asset classes, with underlying fund expense ratios ranging from 0.03% to 0.30%. Algorithms handle rebalancing automatically when allocations drift, and tax-loss harvesting runs daily in taxable accounts.

For 2026, Betterment is refining its portfolio construction: U.S. equity exposure shifts slightly toward large-cap stocks to better align with benchmarks, and non-SRI portfolios are adding an actively managed core bond fund to expand global fixed-income exposure beyond U.S. Treasuries. Betterment reviews and updates fund selections every year based on updated return forecasts and cost efficiency.

BETTERMENT ETF STOCK FUNDS

| Fund Type | Symbol |

| Vanguard U.S. Total Stock Market ETF | VTI |

| Vanguard U.S. Large Cap Value Index ETF | VTV |

| Vanguard U.S. Small Cap Value Index ETF | VBR |

| Vanguard U.S. Mid Cap Value Index ETF | VOE |

| Vanguard FTSE Developed Markets ETF | VEA |

| Vanguard FTSE Emerging Markets ETF | VWO |

BETTERMENT BOND FUNDS

| Fund Type | Symbol |

| iShares Corporate Bond Index ETF | LQD |

| Vanguard U.S. Total Bond Market Index ETF | BND |

| iShares Short-term Treasury Bond Index ETF | SHV |

| Vanguard Short-term Inflation Protected Treasury Bond Index | VTIP |

| Vanguard Emerging Markets Government Bond Index ETF | VWOB |

| Vanguard Total International Bond Index ETF | BNDX |

Fund holdings are representative of Betterment’s Core portfolio and subject to annual updates. Betterment reviews underlying fund selections each year; specific tickers may change.

Betterment Tools

Betterment’s planning toolkit centers on goal-based automation, daily tax-loss harvesting, and cash-sweeping features — built to handle decisions most investors routinely skip.

Goal-Based Retirement Planning

Betterment organizes your investments around named goals — retirement, a home purchase, an emergency fund — each with its own portfolio and time horizon. The retirement planner factors in your savings rate, Social Security estimates, and target spending to project whether you’re on track. Linking external accounts, including 401(k)s, gives the tool a fuller picture of your overall finances.

Tax-Loss Harvesting

Available on taxable accounts, this feature monitors your portfolio daily. When a holding falls below its cost basis, Betterment sells it and buys a correlated replacement ETF — preserving your allocation while banking the tax loss. Betterment reports an average annual tax alpha of 0.77%, though results vary by deposit timing and market conditions. The feature is off by default; enable it in account settings.

Smart Deposit

Smart Deposit automatically sweeps excess cash from your linked bank account into Betterment once your balance clears a threshold you set — keeping idle money invested without manual transfers.

External Account Analyzer

Connect outside 401(k)s and brokerage accounts to compare their expense ratios and allocations against Betterment’s portfolios. The tool flags high fund costs and projects potential outcomes if you consolidated those assets with Betterment.

Socially Responsible Investing

Betterment’s SRI portfolios are available to all customers—Digital and Premium—letting you align your money with environmental, social, and governance (ESG) values at no extra management fee beyond the standard tier rate.

ESG screening filters out companies with records like these, which values-conscious investors typically want to avoid:

| Company | ESG Concern |

| BP | Deepwater Horizon oil spill (2010) |

| Wells Fargo | Fraudulent accounts scandal |

| Exxon Mobil | High carbon emissions and climate lobbying |

What Betterment SRI delivers in 2026:

- Tax-loss harvesting fully supported on SRI taxable goals—and tax-coordinated portfolios apply across account types

- Global diversification maintained—ESG screening tilts holdings without eliminating broad market exposure

- Betterment’s 2026 portfolio refresh updates SRI allocations independently; non-SRI portfolios received a new actively managed bond fund, while SRI strategies retain their ESG criteria

- Standard fees apply—0.25% annually (Digital) or 0.65% (Premium); no SRI surcharge

Betterment Flexible Portfolios

If your preferences differ from Betterment’s default recommendations, Flexible Portfolios let you take more direct control over how your capital is allocated across asset classes.

Betterment Investing Review: Beyond its Core and socially responsible options, Betterment offers Flexible Portfolios for investors who want more say in exactly how their money is invested.

With a Flexible Portfolio, you can adjust the weight of individual asset classes within your chosen strategy and receive real-time feedback on how those changes affect diversification and projected risk. You can also add exposure to non-market correlated assets — including real estate investment trusts (REITs) and commodities — that are not part of the standard Core portfolio.

Standard automation still applies across Flexible Portfolios: automatic rebalancing, Tax-Loss Harvesting, Tax Coordination, and Tax Impact Preview all remain active even when you customize your allocations.

For 2026, Betterment is expanding Flexible Portfolio options by making its new actively managed core bond fund available within the feature, giving hands-on investors broader fixed-income customization. Note that the $100,000 minimum balance requirement applies to the Betterment Premium advisory tier — not to Flexible Portfolios specifically.

Betterment Tax Efficiency

Betterment’s tax strategy focuses on keeping more of your returns through two automated techniques: tax-loss harvesting and tax-coordinated portfolios.

| Type | Capability |

| Tax-Loss Harvesting | YES (daily monitoring on all taxable accounts) |

| Tax-Coordinated Portfolio | YES (assets allocated across taxable and tax-advantaged accounts) |

| TaxMin Lot Selling | YES (prioritizes short-term losses to reduce tax drag) |

TAX-LOSS HARVESTING

Betterment scans your taxable portfolio every day for harvesting opportunities. When a holding falls below its cost basis, the algorithm sells it and immediately buys a correlated replacement ETF — keeping you fully invested while banking the realized loss. Betterment reports an average annual tax alpha of 0.77%, though individual results vary based on deposit timing and market conditions. The system also coordinates across your IRA and taxable accounts to block wash-sale violations that would disqualify a harvested loss.

TAX-COORDINATED PORTFOLIOS

Betterment routes tax-inefficient assets — such as REITs and taxable bonds — into tax-advantaged accounts like IRAs, while placing tax-efficient equity ETFs in taxable accounts. This cross-account optimization works automatically in the background, with no manual rebalancing required on your part.

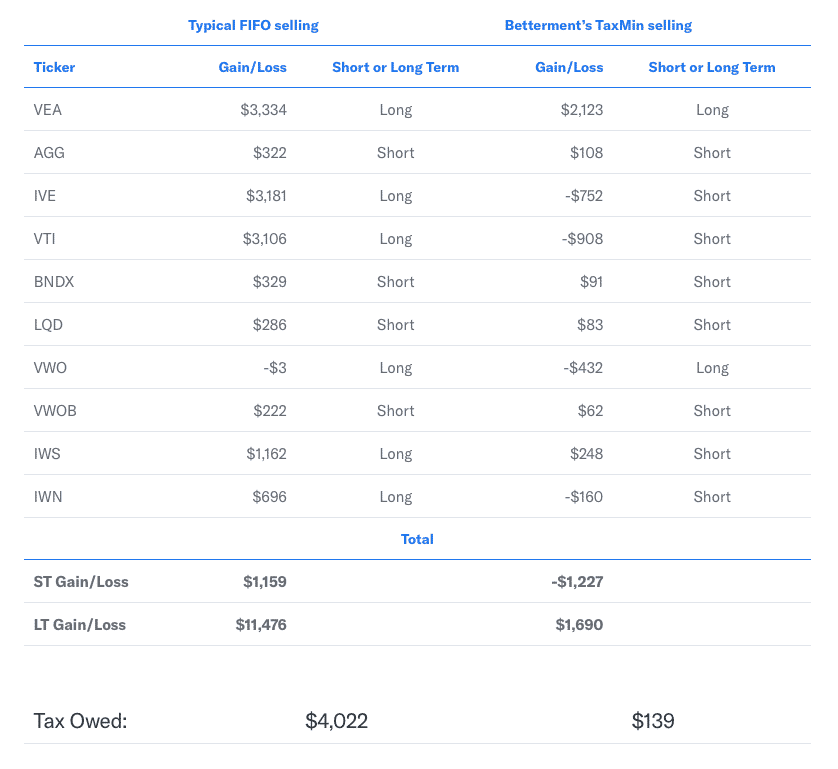

TaxMin Lot Selling

Rather than the standard FIFO (first-in, first-out) method used by most brokers, Betterment’s TaxMin algorithm sells lots in a specific order: short-term losses first, then long-term losses, long-term gains, and finally short-term gains. Each category is fully exhausted before moving to the next, reducing your overall tax liability on every sale.

Tax-Loss Harvesting: Daily Automation and Spousal Coordination

Betterment scans your taxable portfolio every day for tax-loss harvesting opportunities. When a holding drops below its cost basis, the algorithm sells it and immediately purchases a correlated but not substantially identical ETF—locking in a deductible loss without sacrificing market exposure. Betterment reports an average annual tax alpha of 0.77%, though individual results vary based on deposit timing and market conditions.

The feature is included at no extra cost on all taxable accounts, but it is off by default. You must toggle it on in your account settings. Once enabled, Betterment also coordinates activity across your IRA and taxable accounts to block wash-sale violations that would disqualify a harvested loss.

For couples, Betterment extends that same coordination to a spouse’s linked account, treating both portfolios as a single household to optimize after-tax returns together. One important caveat: if you hold the same ETFs at an outside broker—say, VTI at Fidelity—notify Betterment so it can factor in those positions before harvesting, avoiding accidental wash-sale conflicts.

Betterment Pros and Cons

Betterment manages more than $65 billion for over 1 million clients, competing on low fees, automated tax tools, and optional CFP access. The fee structure suits most hands-off investors, though a few cost details are worth understanding before you open an account.

| Betterment Pros | Betterment Cons |

| ✅ Low Management Fee: The Digital plan charges 0.25% annually for accounts with balances above $24,000 or recurring monthly deposits of $250 or more. | ❌ $5/Month Fee on Smaller Balances: Accounts under $24,000 without qualifying recurring deposits pay a flat $5/month — roughly 0.6% annually on a $10,000 balance, well above the headline rate. |

| ✅ Premium CFP Access: Betterment Premium (0.65%/year total) provides unlimited calls with certified financial planners covering retirement planning, Roth conversions, and assets held outside Betterment. | ❌ High Premium Minimum: The $100,000 account minimum for Betterment Premium is a significant hurdle for most retail investors. |

| ✅ No Minimum to Start: A $10 deposit opens a Digital account and starts automated investing in a diversified ETF portfolio immediately. | ❌ $75 Outbound Transfer Fee: Moving assets to another brokerage costs $75 per investing account — a meaningful friction cost if you’re comparing platforms or plan to switch. |

| ✅ Tax-Loss Harvesting: Betterment monitors taxable accounts daily and reports an average tax alpha of approximately 0.77% per year, though individual results vary with deposit timing and market conditions. | ❌ No Direct Indexing: Betterment does not offer direct indexing, which can unlock more granular tax-loss harvesting opportunities on large taxable accounts offered by some rivals. |

| ✅ Tax-Coordinated Portfolios: Automatic asset location across taxable and retirement accounts is designed to improve after-tax returns without any manual input. | ❌ No 529 Plan Support: Betterment does not offer 529 college savings accounts. |

| ✅ Progressive Fee Discounts: Balances above $1 million receive automatic rate reductions — 0.15% on the $1M–$2M tier and 0.10% on amounts above $2M on the Digital plan. | |

| ✅ Retirement Tools: RetireGuide visualizes projected balances, goal progress, and shortfall recommendations in one dashboard, making retirement planning actionable for beginners. | |

| ✅ Socially Responsible Investing: SRI portfolios let you align holdings with environmental, social, and governance priorities at the same fee tier as standard portfolios. |

Where Betterment Shines

Betterment Digital’s 0.25% annual fee is in line with the robo-advisor industry standard, and the $10 starting deposit keeps the door open for new investors. Daily tax-loss harvesting adds real value in taxable accounts — Betterment reports average tax alpha of roughly 0.77% per year. For investors who want human guidance, Betterment Premium at 0.65%/year with a $100,000 minimum delivers unlimited CFP consultations, still a fraction of the 1%+ typically charged by traditional advisors.

What You Need To Know

Smaller accounts pay more in relative terms: a $10,000 balance without recurring deposits triggers a flat $5 monthly fee — roughly 0.6% annually. There is also a $75 outbound transfer fee per investing account if you move assets elsewhere, so factor that into any platform comparison. Betterment still does not offer direct indexing, limiting granular tax-loss harvesting options on large taxable accounts. Finally, some financial advisors caution against holding emergency funds in an investment account: distributions may trigger capital gains taxes that a standard savings account would not incur.

Betterment Review: Fees & Minimums

Betterment’s pricing remains competitive against other robo-advisors and is a fraction of the 1% or more typically charged by traditional financial advisors.

| Category | Fees |

| Account Management Fee – Digital | 0.25% annually (if balance ≥$24,000 or recurring deposits ≥$250/mo.); otherwise $5/month |

| Account Management Fee – Premium | 0.65% annually; $100,000 minimum |

| ETF Expense Ratios | 0.03%–0.30% (fund-level fees; not collected by Betterment) |

| Account Minimum | $0 Digital ($10 to begin investing) $100,000 Premium |

| Outbound Transfer Fee | $75 per investing account |

| Personal Finance Tools | Free (Digital); unlimited CFP access (Premium) |

The Digital plan’s $5/month charge only applies if your balance stays below $24,000 and you haven’t set up recurring deposits of at least $250 per month — a threshold most consistent investors clear quickly. Betterment Premium’s 0.65% fee bundles automated management with unlimited certified financial planner (CFP) access, still well below what a traditional 1% AUM advisor charges. Balances above $1 million receive progressive fee discounts on both plans: 0.15% on the $1M–$2M tier and 0.10% beyond $2M. One cost to watch: crypto portfolios carry a separate 1% annual management fee on top of embedded trading costs.

Betterment Account Types

Betterment directly manages the account types listed below. For accounts held elsewhere—such as an employer 401(k)—Betterment Premium clients can receive CFP guidance, but Betterment does not hold or manage those assets.

| Account Type | Managed by Betterment |

| Individual Taxable | YES |

| Joint Taxable | YES |

| Roth IRA | YES |

| Traditional IRA | YES |

| SEP IRA | YES |

| Rollover IRA | YES |

| Trusts | YES |

| Cash Reserve (High-Yield Savings) | YES — no monthly fees; up to $4M FDIC coverage on joint accounts |

| Checking | YES — no monthly, overdraft, or ATM fees |

| Crypto Portfolio | YES — 1% annual management fee; separate from standard AUM fee |

| Self-Directed Investing (Stocks & ETFs) | YES — added in recent years alongside automated accounts |

| Employer 401(k) | NO (advise only for external accounts; Betterment for Work is a separate employer-facing service) |

| 529 College Savings | NO |

Since the original version of this review, Betterment has meaningfully expanded its product lineup. Cash Reserve, Checking, Crypto portfolios, and self-directed stock trading are now fully integrated, making it possible to consolidate everyday banking, retirement savings, and taxable investing in one platform.

Is Betterment Safe?

Betterment uses bank-level security and offers SIPC protection on brokerage accounts up to $500,000. Cash Reserve balances receive separate FDIC coverage up to $2M for individual accounts and up to $4M for joint accounts across its network of program banks.

| FAQ | Answer |

| Is Betterment SIPC protected? | YES (up to $500,000 per brokerage account) |

| Is Cash Reserve FDIC insured? | YES (up to $2M individual / $4M joint) |

| Does Betterment use 256-bit SSL encryption? | YES |

| Is two-factor authentication used when logging on? | YES |

| Is Betterment regulated? | YES (by FINRA & SEC) |

| Does Betterment receive kickbacks on ETFs used in my portfolios? | NO |

| Will I be charged trading commissions? | NO |

| Is there a fee break for larger balances? | YES (Digital plan: 0.15% on the portion between $1M–$2M; 0.10% above $2M. Same progressive discounts apply on the Premium plan’s 0.65% base fee.) |

Betterment Review Summary

Robo-advisors have leveled the investing playing field—and Betterment remains one of the strongest options in the category. With more than 1 million customers and over $65 billion in assets under management, the platform has cemented its place as a leading choice for automated, goal-based investing.

Should You Choose Betterment?

Betterment suits hands-off investors at nearly any balance. The Digital plan charges $5 per month for smaller accounts, or 0.25% annually once your balance exceeds $24,000 (or you set up $250 or more in monthly recurring deposits). Investors with $100,000 or more can step up to the Premium plan at 0.65% annually for unlimited access to certified financial planners (CFPs).

Core features—automated rebalancing, tax-loss harvesting, and goal-based portfolio architecture—are included on the Digital tier. Betterment reports average annual tax alpha of 0.77% from tax-loss harvesting alone, which can meaningfully offset the advisory fee for taxable accounts. For 2026, the platform is also rolling out portfolio updates that expand bond market exposure and refine equity allocations to better align with current benchmarks.

If you want a low-cost, set-it-and-forget-it investing solution backed by strong automation and tax-efficiency tools, Betterment is very hard to beat.

Free Retirement Guide: Grow Your Wealth Automatically